Why People Choose Annuities for Retirement Protection and Income

Why People Choose Annuities for Retirement Protection and Income

May 20, 2026

By VitalShield Insurance Services | Minneapolis, MN

You worked hard your entire life. You saved. You sacrificed. And now retirement is either here or getting close.

The last thing you want is to outlive your money.

That fear is real. It has a name. It is called longevity risk. And it is one of the biggest financial threats facing retirees today. Social Security helps, but it was never designed to carry the full weight of your retirement. Pensions are nearly extinct. The stock market can swing wildly right when you need stability the most.

That is exactly why millions of Americans turn to annuities.

In this guide, we break down what annuities are, why people choose them, and whether one might be the right fit for your retirement plan.

What Is an Annuity?

An annuity is a contract between you and an insurance company. You put money in, either as a lump sum or a series of payments. In return, the insurance company promises to pay you income, either immediately or at a future date you choose.

Think of it as creating your own personal pension.

Annuities come in several types. Fixed annuities provide a guaranteed interest rate. Variable annuities tie your returns to market performance. And indexed annuities, often called Fixed Indexed Annuities (FIAs), offer growth tied to a market index like the S&P 500, with protection against losses.

Each type serves a different purpose. The key is matching the right annuity to your specific retirement goals.

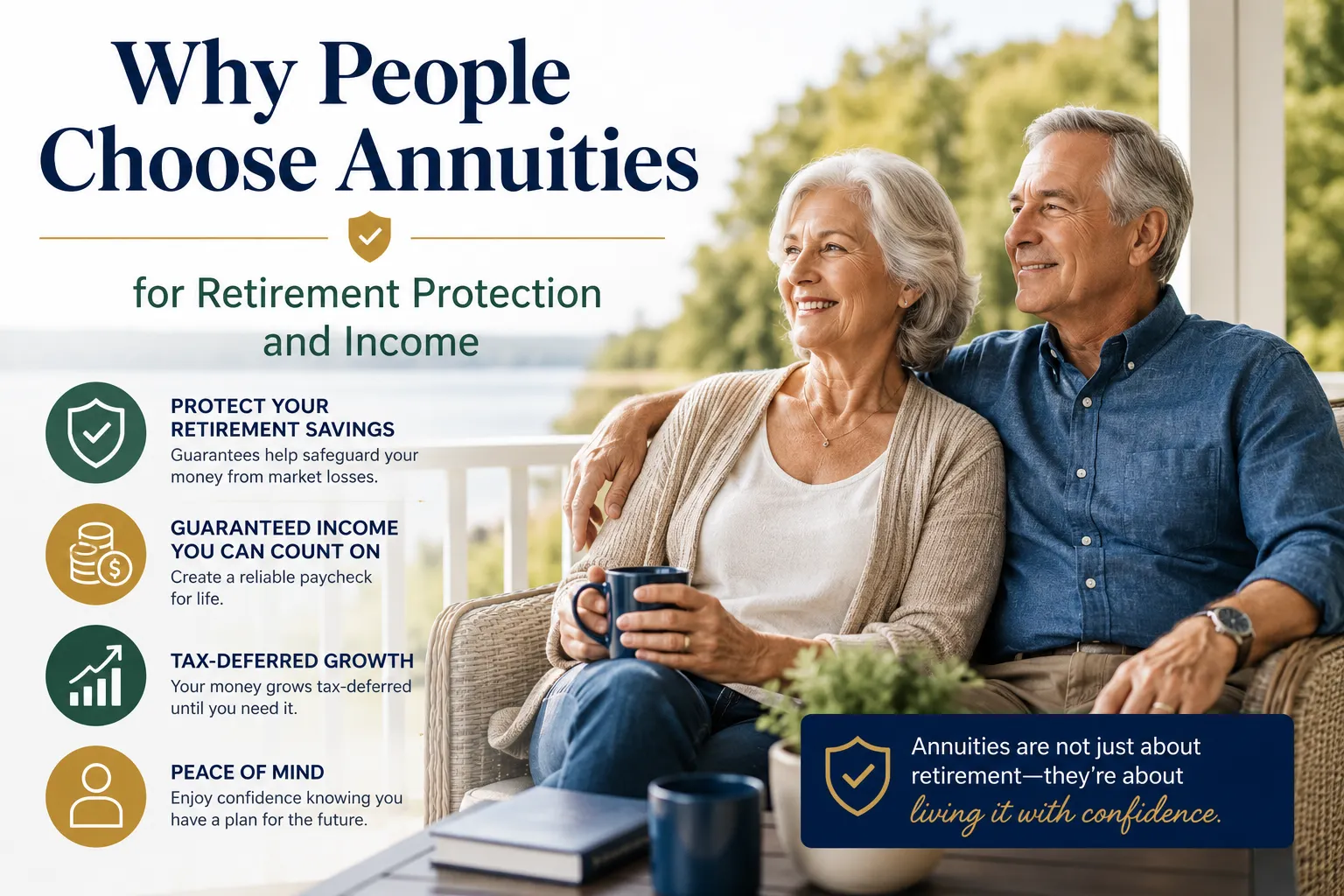

The 5 Biggest Reasons People Choose Annuities

1. Guaranteed Income You Cannot Outlive

This is the number one reason people buy annuities.

No matter how long you live, your income keeps coming. Whether you live to 80 or 100, the check arrives every month. That peace of mind is priceless.

With a lifetime income rider attached to your annuity, you activate a stream of income that lasts as long as you do. You can even set it up to continue for a surviving spouse. This type of protection is called joint-life income, and it ensures your partner is never left without financial support.

Running out of money in retirement is not a small risk. The average 65-year-old today has a 50% chance of living past 85. Many live into their 90s. Annuities are designed specifically for people who plan to live a long life.

2. Tax-Deferred Growth

Money inside a non-qualified annuity grows tax deferred. You do not pay taxes on gains until you take distributions.

This is a powerful advantage. Every dollar that would have gone to the IRS stays in your account, compounding year after year. Over a 10 to 20-year accumulation phase, the difference can be substantial.

For people who have maxed out their 401(k) and IRA contributions, annuities offer another tax-advantaged bucket for retirement savings. There are no annual contribution limits on non-qualified annuities.

3. Principal Protection

Fixed and indexed annuities offer something the stock market cannot: protection against loss.

With a fixed indexed annuity, your principal is not directly invested in the market. If the index goes down, you do not lose money. You simply earn zero for that period. But when the index goes up, you capture a portion of those gains.

For retirees and pre-retirees within 5 to 10 years of retirement, this matters enormously. A 30% market drop can devastate a portfolio at the worst possible time. An annuity shields you from that sequence-of-returns risk.

You cannot afford to recover from a major loss when you are drawing income from the same account.

4. Predictability in an Unpredictable World

Social Security decisions are complex. Medicare costs are rising. Healthcare expenses in retirement average over $300,000 per couple. Inflation erodes purchasing power every year.

Amid all of that uncertainty, an annuity creates one fixed point of certainty: your guaranteed income.

When you know a specific dollar amount hits your account each month no matter what the market does, budgeting becomes simpler. You can plan around it. You stop checking the market every morning hoping your portfolio survived the night.

That psychological benefit is real. Studies show retirees with guaranteed income sources report significantly higher levels of satisfaction and lower levels of financial anxiety.

5. Legacy and Beneficiary Protection

Many annuities include death benefit provisions. If you pass away before you have received all the money you put in, a death benefit ensures your heirs receive the remaining value.

Some annuities allow you to pass the account directly to a named beneficiary, bypassing probate. This can simplify the estate process significantly and ensure your loved ones receive what you intended.

With proper structuring, an annuity can be a meaningful part of your legacy planning alongside life insurance.

Who Is the Best Candidate for an Annuity?

Annuities are not for everyone. But they tend to be an excellent fit for people who:

- Are within 5 to 15 years of retirement or already retired

- Have maxed out other tax-advantaged accounts

- Fear outliving their savings

- Want to reduce dependence on market performance

- Desire a predictable monthly income in retirement

- Have a spouse who would need continued income if they passed first

- Are looking for a complement to Social Security, not a replacement for it

If any of those describe you, a conversation with a licensed annuity specialist is worth your time.

Common Annuity Myths, Debunked

Myth: “Annuities are too complicated.”

Some are. Some are simple. A basic fixed annuity is no more complicated than a bank CD. The key is working with an agent who can explain every feature in plain English, not insurance jargon.

Myth: “I will lose my money if I die early.”

Most modern annuities include return-of-premium provisions or death benefits that protect your principal for your heirs. Read the contract carefully and ask your agent about the specific protections included.

Myth: “Annuities have terrible fees.”

Variable annuities can carry high fees. Fixed and indexed annuities typically have little to no direct fees, though carriers do build their costs into caps and participation rates. Transparency matters. Always ask for a full breakdown.

Myth: “I can’t access my money.”

Most annuities include free withdrawal provisions, typically 10% of the account value per year, without surrender charges. Surrender periods do exist, usually 5 to 10 years, but proper planning accounts for your liquidity needs before placing funds in an annuity.

Fixed Indexed Annuities: The Most Popular Option in Retirement Planning

Among all annuity types, fixed indexed annuities have grown dramatically in popularity for one reason: they offer market-linked growth with downside protection.

Here is how they work in simple terms:

- Your money is not invested directly in the stock market

- The insurance company credits interest based on the performance of an index (like the S&P 500)

- If the index goes up, you earn a portion of those gains, up to a cap or based on a participation rate

- If the index goes down, you earn zero, not negative

- Your principal is protected

Add an income rider, and you also get a guaranteed income stream that begins whenever you choose, typically between ages 60 and 85.

This combination of growth potential, principal protection, and guaranteed income has made FIAs one of the most recommended tools in modern retirement planning.

Questions to Ask Before Buying an Annuity

Before you sign any contract, make sure you get clear answers to these questions:

- What type of annuity is this, and how does it work?

- What is the surrender period, and what are the penalties for early withdrawal?

- What are the annual free withdrawal provisions?

- Is there a guaranteed income rider, and what does it cost?

- How is the death benefit structured?

- What is the financial strength rating of this insurance carrier?

- How is my agent compensated for this sale?

A trustworthy agent will answer every one of these questions without hesitation. If you feel pressured or confused, walk away.

How VitalShield Can Help

At VitalShield Insurance Services, we work with multiple top-rated carriers to find annuity solutions that match your real retirement goals, not a sales quota.

We take time to understand your income needs, your timeline, your risk tolerance, and your legacy goals. Then we present options that make sense for your situation.

We serve clients across Minnesota and Florida, with access to plans nationwide.

There is no cost for a consultation. No pressure. No obligation.

If you are curious about whether an annuity belongs in your retirement strategy, let us have that conversation. You deserve straight answers from someone who puts your interests first.

Schedule Your Free Retirement Income Review

Ready to find out if an annuity is right for you?

Book a Free Consultation with VitalShield https://www.vitalshieldus.com

VitalShield Insurance Services LLC is an independent insurance agency licensed in Minnesota and Florida. We represent multiple carriers to offer unbiased guidance tailored to your needs. Annuity products and features vary by carrier and state. This article is for educational purposes only and does not constitute financial or legal advice. Consult a licensed professional before making any financial decisions.